If 2016 showed that political uncertainty still holds sway over financial markets, 2017 has demonstrated the latter’s surprising resilience. Even as Brexit indecision rumbled on, growth in the eurozone hit its fastest rate in a decade. Meanwhile, as US President Donald Trump failed to pass his tax reforms and threatened to tear up longstanding trade deals, measures of economic confidence in the country reached highs that have rarely been seen since the global financial crisis.

However, there are clouds on the horizon. Global productivity remains low, while income inequality levels are high and continue to rise. The relative stability experienced throughout 2017 could turn out to be little more than a temporary respite if long-term economic issues are not addressed soon.

For businesses, this means viewing the global financial landscape with cautious optimism. Innovative new technologies are emerging that are demanding investment, even as regulatory hurdles threaten to stifle them. Oil prices may have rallied throughout 2017, but economic diversification and renewable energy investment must continue if the impact of price volatility is to be lessened.

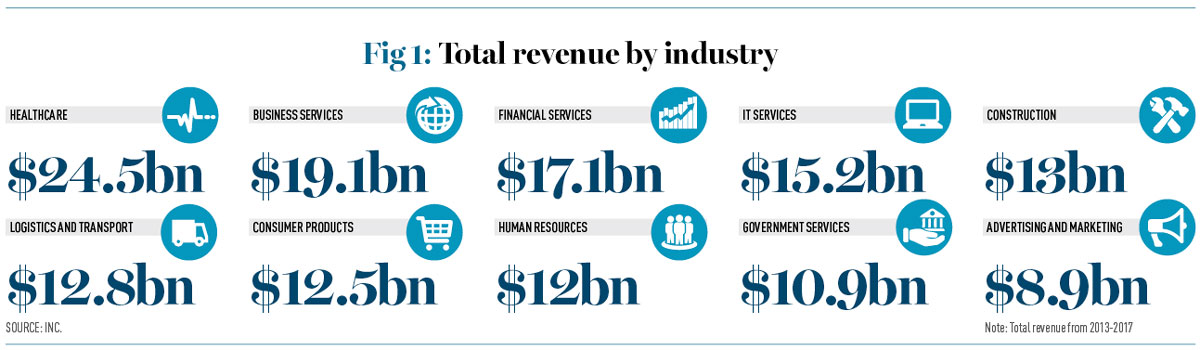

In the World Finance 100, we highlight the firms that have successfully navigated the year’s challenges while simultaneously carving out new opportunities for both themselves and the wider industry. We have put the spotlight on the businesses that have embraced risk without compromising on sustainability. Establishing themselves at the top of their respective industries (see Fig 1), these organisations have demonstrated a commitment to strong leadership, financial discipline and strategic development.

Fiscal intervention

How much of a role central banks should play in a country’s economy is difficult to determine. Even when independent financial institutions are given a clear objective by national governments, such as targeting inflation, it is not always easy to achieve. In the UK, the Bank of England has found that curbing inflation at around the two percent mark is difficult when faced with a weak pound and rising import costs.

The bank’s subsequent decision to raise interest rates for the first time in more than a decade has been criticised as a premature reaction to what is likely to be temporary inflationary pressure resulting from the Brexit vote. There is concern that the increase, and any more increases that may follow, could threaten the country’s growth, which is hardly inspiring as it is.

In the eurozone, however, a subtly different problem is being witnessed. Here, the prospect of monetary tightening also looms large, but in this case it is because of concerns that the economy may be over-stimulated. In October 2017, European Central Bank (ECB) President Mario Draghi confirmed that the ECB would be reducing its asset purchasing programme, but worries over a strong euro and low inflation mean that some doubts remain as to whether this is the right decision.

There is also the long-term question of how economies should respond to future recessions. The traditional method of cutting interest rates is no longer viable when they are already at historic lows. These macroeconomic issues will not be at the forefront of business leaders’ minds, but they should at least be kept in their thoughts considering the financial crisis is still fresh in the world’s memory.

Rules and regulations

Financial regulations are always shifting, closing off loopholes and reacting to new developments. In 2018, one of the most significant regulatory changes to hit the financial sector in a number of years will come into force: an updated version of the Markets in Financial Instruments Directive.

Known as MiFID II, the revamped regulations will be implemented from January 3, 2018 and will introduce new rules that cover every aspect of financial trading in the EU. Institutions will be encouraged to conduct more digital trading in order to take advantage of the regulation’s clearer audit trail, while all electronic communications will now need to be stored for a minimum of five years. Asset managers will also be required to separate their budgets for trading and research.

Finance firms in the EU will need to scrutinise the new regulation to see what changes, if any, they have to implement. Furthermore, they may also want to set aside a fair chunk of time in order to do so, as MiFID II is composed of 1.4 million paragraphs of regulation.

Just a few months after MiFID II comes into force, businesses with EU interests must also ensure that they are prepared for another regulatory change. The General Data Protection Regulation (GDPR) will apply from May 25, 2018. It promises greater control for data subjects and more severe fines for non-compliant companies.

“The relative stability experienced throughout 2017 could turn out to be little more than a temporary respite if long-term economic issues are not addressed soon”With the introduction of the GDPR, the EU is demonstrating that it takes the privacy of its citizens very seriously. The definition of ‘personal data’ has been broadened to include anything that can be used to identify an individual, whether it’s genetic material or a GPS signal. Even pseudonymised data may come under the GDPR’s jurisdiction, depending on how easy it is to discern the individual involved. Organisations must also obtain explicit consent before collecting or processing information, and they must provide complete transparency for their data subjects.

Firms in the financial sector will need to ensure that their processes are aligned with the new ruling and that all members of staff are informed of any corporate policy changes. Organisations located outside the EU should also be aware of the incoming legislation, as it applies to any business that handles data belonging to EU citizens, no matter where in the world they are based.

Fintech ventures

Bitcoin and other cryptocurrencies may not be making mainstream headlines with the same regularity of a few years ago, but blockchain, the technology underpinning them, continues to make waves in the world of finance. No longer a niche technology, blockchain has now been legitimised by a number of established and well-respected financial institutions.

In the first six months of 2017, blockchain companies raised more than $240m of venture capital money, a significant increase when compared with the previous year. Central banks in Brazil, Singapore, India and many other countries are now exploring opportunities related to blockchain. Others are partnering with fintech start-ups to achieve the same results.

Another development in the fintech world that achieved prominence in 2017 was the initial coin offering (ICO) investment method. When conducting an ICO, businesses issue a newly created cryptocurrency in exchange for investor capital. Issues have arisen because ICOs are unregulated and, in contrast with equity-based IPOs, investors do not own any portion of the company. As such, ICOs have become fruitful ground for scammers and are facing legal hurdles in a number of markets.

Our research for the World Finance 100 indicates that although regulations must be updated to prevent new financial technologies from being misused, over-stringent legislation can force such misuse further into the shadows and stifle legitimate innovation. A number of businesses have already used ICOs to crowdfund their projects, finding them to be a fast and transparent way of raising finances.

The past year has demonstrated that knowing when governments should intervene, either in broader monetary policy or industry guidance, is never straightforward. The organisations and individuals that we celebrate as part of the World Finance 100 have successfully navigated a balancing act of their own, pursuing risky new ventures while delivering stability for their customers and investors. They continually raise the standards of their respective industries and bring new opportunities to market. Congratulations to all those that made the final list.